Why Tata Technology Share Price Is Surging in 2026

Tata Technologies Limited (NSE: TATATECH) has seen its search interest spike by over 500% in India in May 2026, making it one of the most-tracked tech stocks on Dalal Street this month. The renewed investor attention comes on the back of strong Q4 FY2026 earnings, a robust order book in engineering R&D services, and the tailwind of India's booming manufacturing and automotive tech sectors.

This article breaks down everything you need to know about Tata Technology's share price, recent performance, and whether it makes sense as an investment in mid-2026.

Tata Technology: What Does the Company Actually Do?

Tata Technologies is a global engineering services company, a subsidiary of Tata Motors. Unlike Tata Consultancy Services (TCS), which focuses on IT services, Tata Technologies specialises in:

- Product Engineering Services: R&D outsourcing for automotive, aerospace, and industrial equipment manufacturers

- Digital Transformation: Helping manufacturers implement Industry 4.0 — IoT, AI, and digital twin technologies

- Education Technology: A growing segment offering vocational training and skilling solutions in partnership with state governments

- EV Tech: Engineering support for electric vehicle development — a major growth driver given the global EV transition

The company serves global OEMs including Jaguar Land Rover, BMW, Volkswagen, and Boeing — giving it diversified, high-quality revenue streams.

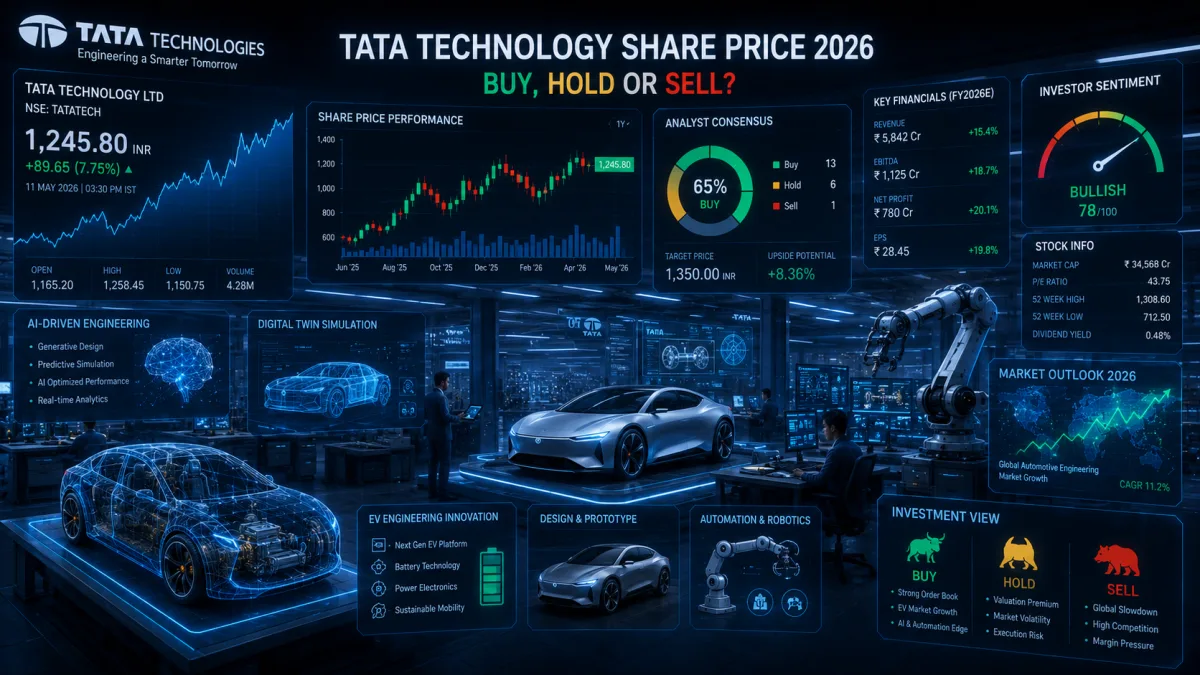

Tata Technology Share Price: Recent Performance

Here's a snapshot of TATATECH's price trajectory:

- IPO Price (Nov 2023): ₹500 per share

- 52-week high (FY2026): ₹1,240

- 52-week low (FY2026): ₹740

- Current price range (May 2026): ₹980–₹1,050

- Market Cap: Approximately ₹40,000 crore

- P/E Ratio: ~38x trailing earnings

The stock had a volatile FY2026 — hitting highs on strong earnings and correcting during broader market selloffs. The current surge in search interest suggests fresh retail and institutional interest is returning.

Q4 FY2026 Earnings: What Drove the Rally

Tata Technologies' Q4 FY2026 results exceeded analyst estimates on multiple fronts:

- Revenue: ₹1,380 crore (up 18% YoY)

- EBITDA margin: 22.4% (expanded by 80 basis points)

- Net profit: ₹185 crore (up 21% YoY)

- Order book: Strongest pipeline in company history, led by EV engineering mandates from European and US automotive clients

Management guided for 20–22% revenue growth in FY2027, citing accelerating demand for EV platform engineering and AI integration in manufacturing.

Key Growth Catalysts for Tata Technology in 2026–27

- EV Boom: As Tata Motors, BMW, and Volkswagen ramp up EV development, engineering outsourcing to Tata Technologies grows in lockstep

- Government Skilling Contracts: State-level ITI and vocational training contracts provide steady, recurring revenue

- Aerospace Recovery: Boeing and Airbus ramp-ups post-2024 supply chain normalisations benefit Tata's aerospace practice

- AI in Engineering: New AI-driven simulation and testing services opening premium pricing opportunities

Risks to Watch

No investment is without risk. Key concerns for Tata Technologies:

- Client concentration: Jaguar Land Rover (a Tata Motors subsidiary) remains a large single-client risk

- Global auto slowdown: Any slowdown in EV adoption or automotive capex cuts could impact the order book

- Valuation premium: At ~38x P/E, the stock is priced for near-perfection; any earnings miss could trigger a sharp correction

- Rupee appreciation: As a dollar-revenue business, a strengthening rupee compresses margins

Should You Buy Tata Technology Shares in 2026?

Tata Technologies occupies a unique position — it's a niche engineering services company with strong Tata Group backing, exposure to the global EV megatrend, and a growing domestic edtech revenue stream. For investors with a 3–5 year horizon, the fundamentals support continued growth.

However, given the current valuation and the recent search-driven attention spike, short-term traders should be cautious about chasing momentum. A systematic SIP approach or waiting for a 10–15% correction to accumulate may offer a better risk-reward profile.

This article is for informational purposes only and does not constitute financial advice. Always consult a SEBI-registered investment advisor before making investment decisions.

For more tech stock analysis and financial technology news, visit our FinTech coverage on TechPopDaily.